(Photo by: himanisdas)

Matt Kurlanzik21st Century FoxDirector, Government Relations Asia |

Yet again, the World Cup proved to be an incredible event with a one-of-a-kind ability to connect and engage with audiences across the globe.With millions of viewers watching matches online, the 2014 World Cup demonstrated the potential of live streaming content; unfortunately, the 2014 World Cup also illustrated that illegal online piracy remains a serious threat to the continued development of online video content and distribution.

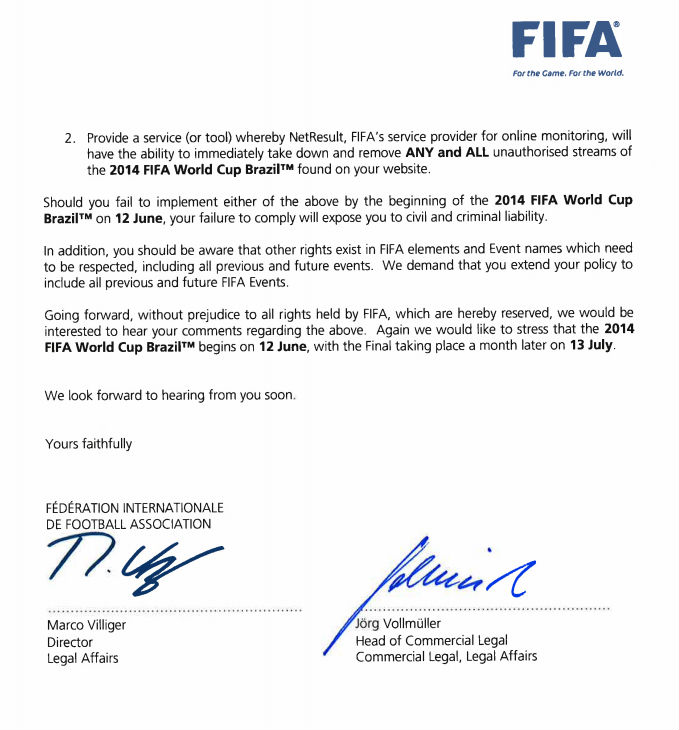

Legal, legitimate options are not the silver bullet The 2014 World Cup broke records for both traditional TV viewing and online streaming. Due to substantial investments in online platforms, websites were able to handle the increased usage and deliver quality video, even with Internet traffic peaking at 6.87 terabytes per second. Despite the wide range of options that World Cup viewers had, millions still turned to illegal live streams of the event. For example, the game between Russia and Belgium drew 471,541 illegal viewers according to Viaccess-Orca, a firm specializing in live stream take down notices. Here in Hong Kong, TVB purchased the rights to 2014 World Cup for HK$400 million (approximately US$52m) and as part of their World Cup broadcast they offered the matches “anytime, anywhere and on demand.” TVB even offered fans a chance to watch games in state of the art 4K, which left viewers ‘over the moon.’ TVB made a strategic decision to invest in the content rights of the World Cup, but despite broadcasting games to multiple devices and offering a number of free broadcasts, many Hong Kongers still turned to illegal, pirated streams online. In addition to these illegal Internet streams, illegal streaming devices, or “black boxes” offered unauthorized broadcasts of World Cup matches. These illegal black boxes were detrimental to TVB’s World Cup broadcast and continue to be a threat to the TV industry in Hong Kong. The prevalence of these unauthorized, illegal streams available online and through streaming devices illustrates that even when operators provide high-quality legal streams of content across multiple devices, piracy remains rampant. Commercial cooperation is necessary for online video to prosper Prior to the start of the World Cup, FIFA, the organizer and main beneficiary of the World Cup, issued a strongly worded letter that threatened pirate websites with civil and criminal liability lawsuits. While some commented that this is “above and beyond” common takedown procedure, most companies in the online video ecosystem attempted to comply and work with FIFA. In the United States, Google worked with World Cup rights holder ESPN and reached a deal where the search engine directed users to the ESPN website or streaming app to show licensed and authorized highlights of the game. The financial terms of the deal between Google and ESPN were not disclosed, but whether or not ESPN had to pay Google to feature authorized video clips, it is refreshing to see this type of cooperation from Google. It is also encouraging to see that Internet search engines can take reasonable measures to address the queries of the user while at the same time acknowledge the authorized rights holder. This continued type of action is essential for legitimate online content to grow and thrive. Univision, a Spanish-language channel based in the U.S., is another example of how streaming the World Cup can be a wise strategic investment. Univision spent over US$325 million for the Spanish language rights to the 2010 and 2014 World Cup, and has continued to invest in technology to deliver the World Cup into American homes seconds faster than its competitors. Univision also offered free streaming to American viewers on multiple devices including their PCs and cellphones. All of these factors, and the fact that Univision reached nearly 81 million viewers, up 34% from 2010, in its World Cup broadcast caused the New York Times to call Univision the Biggest Scorer in the World Cup. The World Cup showed that an innovative tech giant such as Google can play a helpful role in upholding content rights. Hopefully these tech innovators will continue their commitment to protecting content rights, but their sustained cooperation remains unclear. Social media delivers tremendous exposure and raises new questions Social media continues to impact how we consume and interact with video content, in particular live broadcast events like the World Cup. It should not be a great surprise, but there were record numbers of social interactions related to the 2014 World Cup, with an estimated 350 million Facebook users posting 3 billion World Cup related conversations and 672 million World Cup related tweets. In the Final alone, 88 million Facebook users had 280 million interactions and Twitter users sent out 32.1 million tweets, or 618,725 tweets per minute. Facebook and Twitter were not the only social media players to participate in the World Cup action. The users of Vine, the Twitter-owned social networking service that utilizes six second video clips, promoted all types of short videos related to the World Cup. Most operators had no issue with Vine videos showing fans celebrating or other World Cup related clips, but many Vines were showing the most dramatic game action, such as goals, free kicks and yellow cards. The trouble with these “social media” clips and the websites that promoted them is they were not authorized to distribute these video clips. Also, many of the rightsholders (e.g. TVB or Univision) offered programming designed to showcase these valuable highlights. As a result, FIFA and various rightsholders requested that Vine videos with unauthorized content be taken down. These Vine highlights further demonstrate how new digital technologies and social media services can generate exposure and promote fan interaction, but at the same time may inhibit the growth of an online video ecosystem by ignoring content rights. Piracy continues to be an obstacle to online video innovation and distribution From content to distribution, this is an exciting time to be involved in the online video space. Companies are continuing to make strategic investments to capitalize on growing consumer demand for online video. The 2014 World Cup emphasized the opportunities and challenges that currently exist in online video, and it showed that affordable, legitimate alternatives are not a panacea to piracy. A variety of stakeholders: governments, rightsholders, distribution platforms and tech innovators, need to show a committed effort to reducing piracy to allow online video to succeed, and additional measures need to be available to remove and create disincentives for websites offering illegal, unauthorized content. This will allow legitimate players to flourish and will encourage more investment. The 2014 World Cup shows the potential of streaming content but plenty of work remains to ensure this potential is realized.

|

{kind=link}